Dump Trump’s unaffordable N.Y. real estate tax break, aka 421-a

By Latrice Walker and Kevin Parker, New York Daily News

Latrice Walker is a Brooklyn assemblywoman and Kevin Parker is a Brooklyn state senator. They authored this article, which originally published March 23, 2017 on the New York Daily News.

If you want to know who really benefits from the real estate tax abatement known as 421-a, look no further than a lawsuit filed by then-developer Donald Trump 36 years ago, which to this day inflicts this unaffordable burden on New York City, costing $1.3 billion this year alone in foregone property taxes.

If you want to know who really benefits from the real estate tax abatement known as 421-a, look no further than a lawsuit filed by then-developer Donald Trump 36 years ago, which to this day inflicts this unaffordable burden on New York City, costing $1.3 billion this year alone in foregone property taxes.

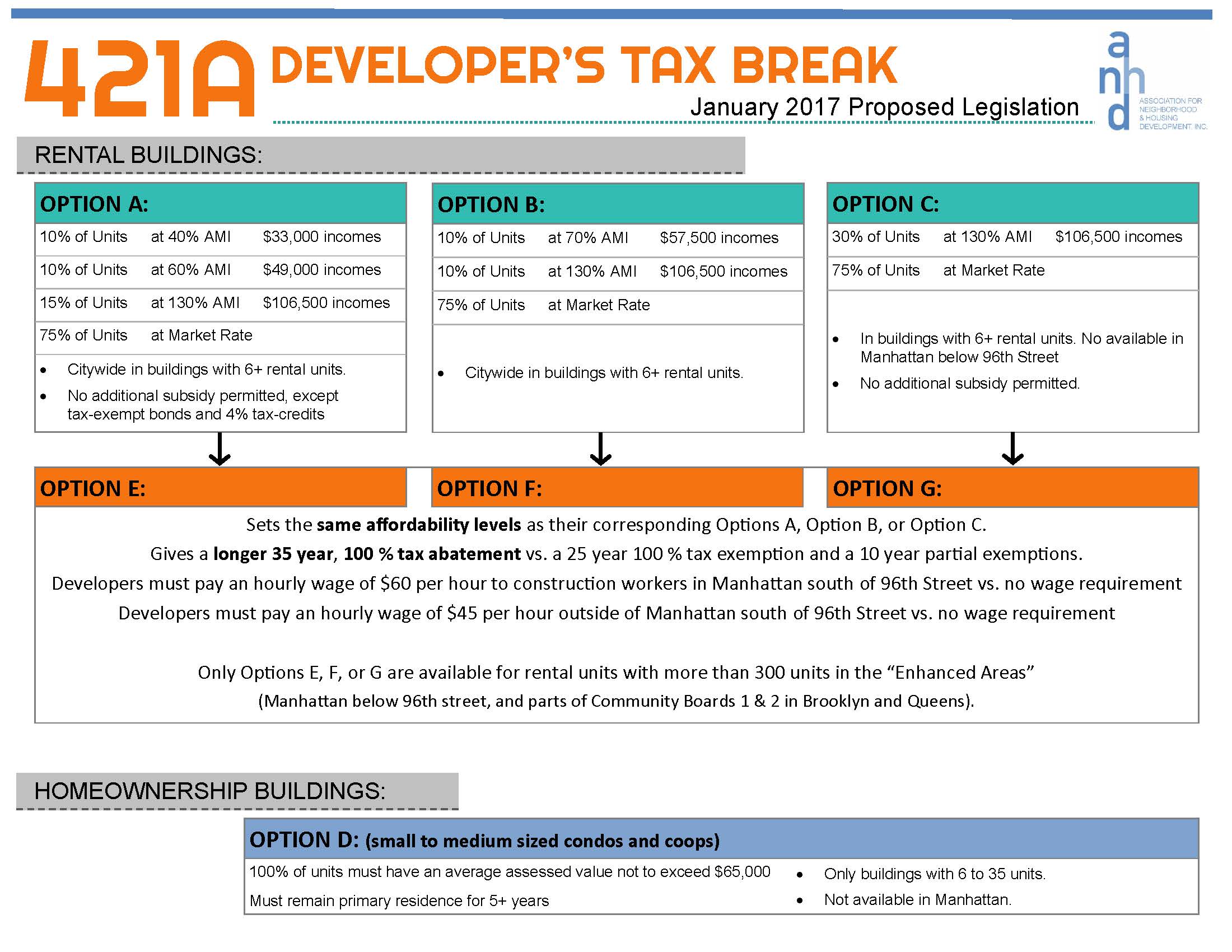

Now, Albany is considering bringing back the 421-a tax exemption, which expired last year in a political impasse. And this time, proposals would make the program even more expensive.

New York is facing a human services crisis as President Trump slashes the federal budget. The cuts to housing programs alone will add up to hundreds of millions of dollars, which will become a fiscal crisis as local government confronts the impossible task of filling those budget holes.

In the face of Trump’s cuts, we must think twice before giving away our tax revenues in a massive tax exemption created by Developer Trump.

The original 421-a tax exemption was created in the 1970s when the city economy was in crisis, and was designed to encourage new development in locations that were vacant or underutilized.

But in 1980, Trump bought the iconic Bonwit Teller department store on Fifth Ave., with plans to knock it down and build Trump Tower. Then, as now, Trump did not want to pay his taxes.

Told by Mayor Ed Koch that the Bonwit site could not qualify for a 421-a tax break, Trump and his lawyer – the infamous Roy Cohn – sued the city. In the end, they won a tax exemption worth $50 million for the extravagant Trump Tower, packed with luxury condominiums.

More importantly, Trump’s lawsuit established that all new development, even luxury projects, would be automatically eligible for the 421-a exemption. Koch said then: “The Court of Appeals has found that some of the most expensive and luxurious accommodations, not only in the United States but in the world, are entitled to a tax break. Does that make sense? Not to me.”

And not to most New Yorkers, either.

We never fixed this costly mistake, and now all these years later, with New York City one of the hottest real estate markets in the world, restoration of the 421-a program would continue to offer an automatic tax exemption. Most luxury developers in our city have paid little to no property taxes for decades, with their profits effectively subsidized by the public.

Even as the city added requirements to include affordable housing in some buildings receiving 421-a, at its core it remained a subsidy for luxury developers. The Association for Neighborhood and Housing Development found that of the 152,402 residential units built under the program, only 12,700 were affordable.

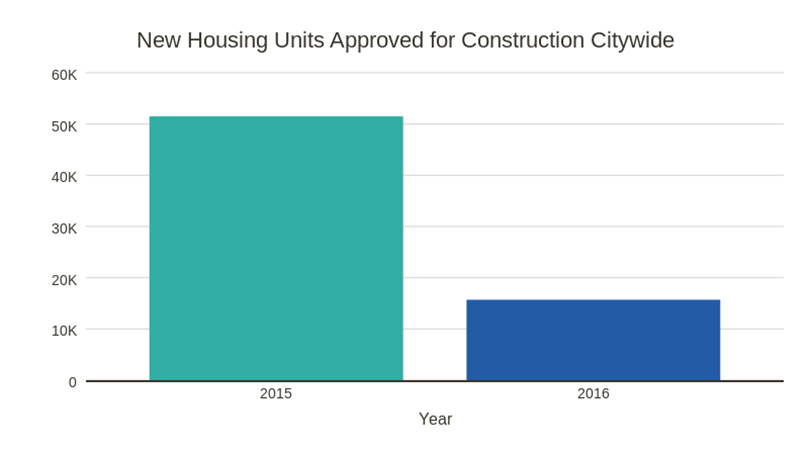

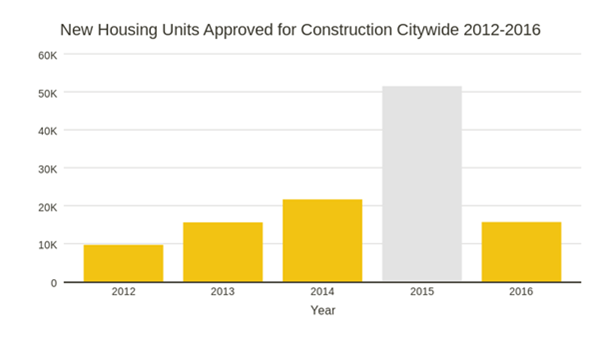

With 421-a suspended for the past year, evidence has mounted in the meantime that the program may not even accomplish the most basic presumed purpose of encouraging new development. The number of new apartment building construction permits across the city is back up to previous levels, suggesting not only that the tax break was not needed, but that it may have been hindering development by inflating land prices.

Now, the real estate industry wants to bring the expired 421-a program back, and expand the benefit to make it even more costly, adding hundreds of millions of dollars to the expected annual cost to the city.

Meanwhile, Trump is planning unprecedented federal budget cuts that target essential services for New Yorkers. To respond to these budget cuts, the city will need to rely on exactly the money that we are giving away to the luxury real estate industry for Developer Trump’s tax exemption.

New Yorkers have shown up at the polls and in the streets to reject Trump’s policies. And New York’s elected officials have shown leadership by saying that our state will be a sanctuary of good policy to protect our residents.

It’s time for us to say no to Trump. His real estate tax exemption shouldn’t be rammed through the Albany budget process, but instead should be negotiated separately and apart from the budget, which is due April 1. We must take the time to get the details right.

The problems with the 421-a exemption are too expensive to ignore. For every dollar the program spends, only 11 cents go toward affordable housing, with the rest subsidizing luxury development. No one would call that a well-designed program.

It didn’t start out that way, and we have Donald Trump to thank for the exemption’s bad turn.

Let’s look at it in the light of day. Let’s decide who should benefit, and what it should cost. Let’s get it right this time.